在ACCA考試中,F3階段中的“合并報表引入”知識點經常都會出現在每年的考卷上,該考點內容也存在著一定難度,今天會計網就幫大家進行梳理,我們來看看吧。

高頻考點解析")

合并:把兩個及以上的公司作為一個整體來展示他們的財務狀況和經營情況。

原因:母公司通常擁有子公司絕大部分的股票份額,產生了控制權,要整體表現公司狀況。

從法律角度講:母公司和子公司是獨立的主體,要做獨立的公司報表,而合并報表是將所有的經濟交易作為一個整體公司來進行表達。

基本原則:假設P是母公司,S是子公司,P擁有S 80%的股票

1、add together:把相同項相加。P的PPE價值100W,S的PPE價值50W,合并的PPE價值是150W(雖然只擁有80%,但是母公司可以控制子公司所有的資產,所以加100%的子公司的資產切記不是100W+50W*80%=140W)

2、 cancellation of like items internal to the group:內部交易的抵消。假設P公司有應付賬款100W ,S 有應收賬款50W。P在S賒購10w存貨,P報表有欠S應付賬款10W,S報表有P10W的應收賬款。那么在合并報表中應收賬款應該是50W-10W,應付賬款應該是100W -10W(本質上商品還是在自己的手中,沒有產生轉移)

3、owned everything then show the extent to which you do not own everything:母公司像擁有子公司一樣去控制子公司。母公司能夠完全控制子公司的所有資產和負債的。例如上面的150W的PPE一樣。

Subsidiary:子公司

相關的準則:

IAS 27 Separate financial statements *

IAS 28 Investments in associates and joint ventures *

IFRS 3 Business combinations *

IFRS 10 Consolidated financial statements *

相關的概念要牢記,學習,理解以及應用。例如:Control, Power, NCI少數股東權益, Subsidiary, Parent, Group集團公司, Consolidated financial statements合并報表。

投資占比:

Subsidiary:>50%的股票。一般而言control,>50%voting power 超過一半的投票權, power to govern the financial and operating policies 有權力管理公司的日常活動, power to appoint or remove a majority of members of the board of directors 有權任命或移除董事會的大部分成員。

Associates:20%-50%之間的份額,significant influence using the equity method 通常使用權益法進行計算,IAS28 requires 'power to participate', but not to 'control' 有權參與但是無權控制(參與公司的日常活動和財務等決策)董事會里面有代表,Participation in the policy making process 參與方針決策的制定

Trade investments,僅僅是為了分紅或者分利潤。記錄方式:Trade investments are simply shown as investments under non-currentassets in the consolidated statement of financial position of the group.

插播:equity method權益法(聯營公司的計量方法)

基本原則:假設A是associate,P是被投資公司。不管P公司是否分配earnings as dividends,A公司總會把P的稅后利潤加在自己的報表中。P Co achieves this by adding to consolidated profit the group'sshare of A Co's profit after tax.

還有一個值得注意的點:如果聯營公司分紅之后,收到了現金,那對應的投資就會減少,例如:聯營公司初始投資100W,本年屬于聯營公司的利潤是20W,收到了10w的現金,那么在年底的時候associate的投資值是100+20-10=110W(權益法的實質核心)。

注意: 在SPL中,與控制子公司(記>50%的所有科目)不一樣,權益法中不記錄sales revenue,cost of sales等其他科目,不是一行一行加,而是只記錄profit after tax。

Under equity accounting, the associate'ssales revenue, cost of sales and so on are not amalgamated with those of thegroup. Instead, only the group share of the associate's profit after tax isadded to the group profit.

來源:ACCA學習幫

Worldwide famous‘Toyota pioneered lean practices’crashed and burned in early 2010,which changed the fate of the world top one automobile manufacturer and also rang the alarm bell to all the finance and operation executives that how to avoid Toyota tragedy while implementing lean finance into production.

As the lean approach percolates into ever wider circles of operations,it ceases to be about best practice and starts to become a part of the fabric of doing business.The important thing,in the heat of competition,will be how well companies implement them and averse the follow-up risks,which caused by the diversity of cultures,infrastructures and environments.

This training aims to look at wider ranging operational excellence programs and the methods of successful implementation.It is also more about building the energy and engagement of employees from the shop floor and the office pool upward,tapping into their ideas,focusing them on constant problem solving,and keeping them open to change and flexibility.

Learning how companies like Boeing,Parker Hannifin,Siemens,Messier Dowty and hosts of smaller firms are revolutionizing accounting,control and measurement processes

The first systematic lean program about the specifics of adapting financial systems to better serve lean operations by the world leading lean authority

Providing accurate,timely and understandable information to motivate the lean transformation throughout the organization,and for decision-making leading to increased customer value,growth,profitability,and cash flow

Using lean methods to eliminate waste from the accounting processes while maintaining thorough financial control

Supporting the lean culture by motivating investment in people,providing information that is relevant and actionable,and empowers continuous improvement at very level of the organization

Developing action plans for implementing Lean Accounting methods in participating companies considering the existing defense industry structural barriers

Learning the approach of how to design and measure work to achieve business objectives to implement your lean system design

Helping the design of a radically new way of the processes and savagely eliminating wastes from it

Putting performance measurement on a different level

Reducing customer wait times and creating value to them by kinds of tools

Executive Leaders,Financial Professionals,Lean Specialists

Financial Directors,Financial Managers,Accountants

Senior Managers in Operations,Product,Procurement,Sales,and Marketing,etc.

Highly recommending to bring a small group or team to the workshop to maximize the benefits

Lean Introduction

Five Principles of Lean Thinking

New lean methods of accounting,control&measurement

Box Score

The Structure of Box Score

Box Score implementing in lean accounting to prioritize the lean improvement projects

Value Stream Management

The importance and helpfulness of value streams

A standard method for determining the value stream flows

Flows implementing for developing the best value stream organization

Group Work:Design a value stream structure for a company making values and manifolds

Lean Performance Measurements

Lean measurements‘Starter Set’

‘Lean Performance Measurement Linkage Chart’

Changing‘command&control’management style to a lean management style

Value Stream Accounting

Value streams as the primary cost objects

Collecting information of summary,direct value stream revenue and cost

Creating a‘Plain English’income statement

Exercise

Value Steam Capacity

Value steam map

Capacity model

Value stream capacity usage and analysis

Exercise

Decision Making

Box Score decision-making templates

Effective decision making

Exercise

Transaction Elimination

Identifying and eliminating the wasteful transactions

Transaction Elimination Maturity Path Matrix

Lean Accounting‘Footprint’Chart–current&future state

Documenting the changes

Exercise

Box Score in an Administrative Process

Box Score for monitoring and improving the process

Radical improvement in an account payable process

Implementation of Basic Lean Accounting

Approach to the implementation of basic lean accounting

想了解最新詳細課程大綱及資料,點擊網頁左側的在線咨詢圖標,與在線老師交流。

ACCA考試為全英文考試,考試涉及較多財會詞匯,考生需要掌握常見的英語詞匯,才能更好的備考ACCA考試,以下分享部分ACCA考試常見英語詞匯,具體如下:

ACCA考試常見英語詞匯

1、Accelerated Depreciation加快折舊:

任何基于會計或稅務原因促使一項資產在較早期以較大金額折舊的折舊原則

2、Accident and Health Benefits意外與健康福利:

為員工提供有關疾病、意外受傷或意外死亡的福利。這些福利包括支付醫院及醫療開支以及有關時期的收入。

3、Accounts Receivable(AR)應收賬款:

客戶應付的金額。擁有應收賬款指公司已經出售產品或服務但仍未收取款項

4、Accretive Acquisition具增值作用的收購項目:

能提高進行收購公司每股盈利的收購項目

5、Acid Test酸性測試比率:

一項嚴謹的測試,用以衡量一家公司是否擁有足夠的短期資產,在無需出售庫存的情況下解決其短期負債。計算方法:(現金+應收賬款+短期投資)/流動負債

6、Act of God Bond天災債券:

保險公司發行的債券,旨在將債券的本金及利息與天然災害造成的公司損失聯系起來

7、Active Bond Crowd活躍債券投資者:

在紐約股票交易所內買賣活躍的定息證券

8、Active Income活動收入:

來自提供服務所得的收入,包括工資、薪酬、獎金、傭金,以及來自實際參與業務的收入

9、Active Investing積極投資:

包含持續買賣行為的投資策略。主動投資者買入投資,并密切注意其走勢,以期把握盈利機會

10、Active Management積極管理:

尋求投資回報高于既定基準的投資策略

11、Activity Based Budgeting以活動為基礎的預算案:

一種制定預算的方法,過程為列舉機構內每個部門所有牽涉成本的活動,并確立各種活動之間的關系,然后根據此資料決定對各項活動投入的資源

12、Activity Based Management以活動為基礎的管理:

利用以活動為基礎的成本計算制度改善一家公司的運營

13、Activity Ratio活動比率:

一項用以衡量一家公司將其資產負債表內賬項轉為現金或營業額的能力的會計比率

14、Actual Return實際回報:

一名投資者的實際收益或損失,可用以下公式表示:預期回報加上公司特殊消息及總體經濟消息

15、Actuary精算:

保險公司的專業人員,負責評估申請人及其醫療紀錄,以預測申請人的壽命

16、Acquisition收購:

一家公司收購另一家公司的多數股權

17、Acquisition Premium收購溢價:

收購一家公司的實際成本與該公司收購前估值之間的差額

18、Affiliated Companies聯營公司:

一家公司擁有另一家公司少數權益(低于50%)的情況,或指兩家公司之間存在某些關聯

19、Affiliated Person關聯人士:

能影響一家企業活動的人士,包括董事、行政人員及股東等

20、After Hours Trading收盤后交易:

主要大型交易所正常交易時間以外進行的買賣交易

21、After Tax Operating Income-ATOI稅后營運收入:

一家公司除稅后的總營運收入。計算方法為將總營運收入減稅項

22、After Tax Profit Margin稅后利潤率:

一種財務比率,計算方法為稅后凈利潤除以凈銷售額

23、After The Bell收盤鈴后:

股票市場收盤后

24、Agent代理人:

1.為客戶進行證券買賣的人士或機構

2.持有銷售保險許可證的人士

3.代表證券經紀行或發行人向公眾出售或嘗試出售證券的證券銷售人員

25、Agency Bonds機構債券:

由政府機構發行的債券

26、Agency Cross交叉代理人:

一項由一名代理人同時代表買方與賣方的交易,也稱為撍卮砣藬“Dual Agency”。

27、Agency Problem代理問題:

債券人、股東及管理人員因目標不同而產生的利益沖突

28、Agency Securities機構證券:

由美國政府支持的企業發行的低風險債務

29、Aggressive Accounting激進會計法:

不當地編制損益表以取悅投資者及提高股價

30、Aggressive Investment Strategy進取投資策略:

投資組合經理嘗試爭取最高的回報。進取的投資者把較高比重的資產投入股票,比重較其他風險較低的債務證券要高

31、Alan Greenspan格林斯潘:

格林斯潘博士是美國聯邦儲備局監理會的主席。他將于2004年6月20日完成第四個四年任期。格林斯潘博士也聯邦儲備局主要貨幣政策制定組織聯邦公開市場委員會的主席

32、Allotment配股:

首次公開上市中向各承銷機構分配,容許其出售的股份。其余股份會分給其他取得上市股份出售權的證券公司

33、Allowance For Doubtful Accounts呆賬準備金:

公司對可能不能收到的應收賬款的預測,這項數據將紀錄在公司的資產負債表上

34、American Depository Receipt(ADR)美國存托憑證:

一份美國存托憑證代表美國以外國家一家企業的若干股份。美國存托憑證在美國市場進行買賣,交易程序與普通美國股票相同。美國存托憑證由美國銀行發行,每份包含美國以外國家一家企業交由國外托管人托管的若干股份。該企業必須向代為發行的銀行提供財務資料。美國存托憑證不能消除相關企業股票的貨幣及經濟風險。

美國存托憑證可在紐約股票交易所、美國股票交易所或納斯達克交易所掛牌上市

35、American Depository Share(ADS)美國存托股份:

根據存托協議發行的股份,代表發行企業在本土上市的股票

36、American Option美式期權:

可在有效期間隨時行使的期權

37、American Stock Exchange美國股票交易所:

美國第三大股票交易所,位于紐約,處理美國交易證券總額的10%

38、Amortization攤銷:

在一段期間分期償還債務

在一個特定時期資本開支的減少。與類似相似,是一種衡量長期資產,例如設備或建筑物在特定期間價值的消耗

39、Analyst分析員:

具備評估投資專長的金融專業人員,一般受聘于證券行、投資顧問機構或共同基金。分析員對不同的證券作出買入、賣出或持有的建議。為了提供全面的研究分析,分析員一般會專注于不同的行業或經濟板塊

40、Angel Investor天使投資者:

向小型初始企業或創業者提供創業資金的財務投資者

41、Annualize年度化:

1.將不足一年的回報率轉為全年回報率

2.將不足一年的稅務期轉為每年一度年度化

42、Annual General Meeting(AGM)年度股東大會:

必須每年舉行一次的股東會議,指在向股東通報公司的決策與工作

43、Annual Report年報:

一家公司每年一度的財務營運報告。年報的內容包括資產負債表、損益表、審計師報告以及公司業務的概要

44、Annuity年金:

在特定期間定期定額支付的款項

45、Annuity Due即付年金:

需要即時支付,而不是在期末支付的年金

46、Anti-dilution Provision反攤薄條款:

期權或可轉換證券的一項條款,用以保障投資者,不會由于未來公司以較低價格(低于有關投資者支付的價格)發行股份而被攤薄

47、Anti-takeover Measure反收購措施:

企業管理人員長期或不時采取,防止或延遲被惡意收購的措施

48、Anti-takeover Statute反收購法規:

旨在防止或延遲惡意收購的一套美國法規。每一州的法規細則有所不同,一般只適用于在州內注冊成立的公司

49、Anti-trust反壟斷法:

美國的反壟斷法適用于所有行業及所有層面的業務,包括制造、交通、分銷及促銷。法律禁止多種對交易造成妨礙或限制的行為。非法行為包括聯合控制價格、可能減弱個別市場競爭動力的企業合并、意圖實現或維持壟斷勢力的掠奪性行為

50、APICS Business Outlook Index

APICS(美國生產及庫存控制協議)商業前景指數:

美國全國性制造業指數,每月對多家制造業企業進行調查。若指數高于50,表示行業正在擴展,若低于50,則表示行業正在萎縮

51、Appraisal價值評估:

對一項物業或業務價值的意見

52、Appreciation升值:

資產價值上升

53、Arbitrage套匯:

同時買入及賣出證券,意圖從差價中獲利,在一般于不同的交易所或市場進行買賣

54、Arbitrage Bond套匯債券:

市政府在市政府現有高評級證券買回日期前發行的低評級債務證券

55、Arbitrage Pricing Theory(APT)套匯定價理論:

是資本資產定價模式以外的另一個選擇,主要分別在于其假設及對資產相關風險因素的詮釋

56、Arbitrage Trading Program(ATP)套匯交易理論:

同時買入股票指數期貨及相關股份的交易計劃,旨在從差價中獲利(市場套匯)

57、Arbitration仲裁:

對爭議的非正式聽證,其間一組由公正委員會選出的人士(一般為三名)對爭議作出裁判。在做出判決會,不設進一步上訴的機制

58、Arms Length Transaction公平交易:

一項產品的買方與賣方獨立進行交易,互相之間并無任何關系

59、Asian Option亞洲式期權:

回報根據相關證券在特定期間的平均價格而定的期權

60、Ask(Price)買方叫價:

賣方愿意接受的證券價格,也稱為要約價格

61、Assessed Value評估后價值:

一項房地產在稅務上的預測價值

62、Assessor估價人:

決定一項房地產在稅務上價值的地方政府官員

63、Asset資產:

個人或一家企業擁有、具有經濟價值的任何物品。資產也是資產負債表上的一個重要項目,顯示公司擁有的價值

企業買入資產以提高公司的價值或促進業務

64、Asset-Backed Security資產抵押證券:

由資產相關票據或應收賬款,而不是房地產為擔保的證券

65、Asset Allocation資產分配:

將一個投資組合分為不同資產種類的過程,主要資產種類包括債券、股票或現金。資產分配的目的在于通過分散投資減低風險

66、Asset Allocation Fund資產分配基金:

一種將投資資產分為債券、股票及其他證券的共同基金,目的在于回報最大化及風險最小化

67、Asset Coverage Ratio資產償付比率:

評估一家企業在扣除所有負債后以資產償付債務的能力,計算方法為:

資產償付比率=[總資產賬面值-無形資產-(流動負債-短期債務)]/未償還債務總額

68、Asset-Liability Management資產負債管理:

企業協調資產及負債管理的措施,以賺取適當的回報

69、Asset Management資產管理:

1.企業管理其財務資產,以實現最高的回報

2.在一家金融機構開設戶口,以享有支票服務、信用卡、記賬卡、保證金貸款、自動將現金結余投入貨幣市場基金以及證券經紀服務

70、Asset Play資產隙:

估值不當的股票,其合并資產價值高于總市值,以而具有吸引力

71、Asset Redeployment資產重新配置:

將公司的資產重新進行策略分配,以提高盈利能力

72、Asset Swap資產互換:

與單純掉期結構相似,主要分別在于潛在的掉期合約。互換的是固定及浮動投資,而不是一般的固定或浮動貸款利率

73、Asset Turnover資產周轉率:

每一單位金額資產產生的營業額。計算方法為:資產周轉率=總營業額/總資產值

74、Asset Valuation資產估值:

評估一個投資組合、一家企業、一項投資或資產負債表項目當時價值的過程

75、Assets Under Management管理資產額:

一般為一家投資公司代表投資者管理資產的市場價值

76、Assignment轉讓:

將要一項權益或物業轉給另一名人士或另一項業務

77、At the Money到價:

一項期權到價指該期權的行使價格相等于相關證券的市場價值

78、ATP套匯交易理論:

同時買入股票指數期貨及相關股份的交易計劃,旨在從差價中獲利(市場套匯)

China’s rise as the most important global M&A market and the almost dramatic increase of Chinese outbound M&A activities signals a sea change of opportunities and pitfalls.As witnessed by the landmark deal between Lenovo and computer giant IBM in 2005,M&A transactions are expected to gather pace as China prepares itself to become an economic superpower.While the central government has somewhat revamped opaque regulations,Mergers&Acquisitions in China:Law and Practice lends much needed clarity by providing a structured introduction to the legal aspects of China’s M&A regime.

The downturn may present many acquisition opportunities,but which fit best with your long-term business strategy?Leading strategic planners will describe how to develop an effective investment strategy,identify potential targets,and efficiently evaluate opportunities.Through this training you will explore how to identify and assess strategic targets,evaluate investment opportunities,navigate today’s deal hurdles,and successfully integrate an acquired business to deliver real results and real value.

Ensuring the realization of the M&A purpose

Deeply analysis on the hottest topics of M&A

Understanding the obstacles of Chinese corporations to do the strategic merge&acquisition

Learning the laws and regulations involving in the merge&acquisition activities

Controlling the risks when formulating a merge&acquisition strategy

Developing M&A deal negotiation skills

Gaining knowledge of target sourcing and driving success in the down market

Advancing in evaluation models and methods

Improving assessment of risk

Obtaining strategies of finance in M&A

CEO,VP,Director,GM,Head and Manager of

Strategic Planning、Finance

Corporate/Business Development

M&A/Legal

Corporate development strategy vs.M&A strategy

Stable development strategy

Defense strategy

M&A categories

Transaction valuation

M&A Financing methods

Case studies

Ensuring the new business conforms to company's objectives

Differentiating Transaction Success&Deal Success

Understanding the main factors for value creation

Reorganizing,reconstructing and adjusting the business system

Recommendation for PMI(Post Merger Integration)strategy

Strategic M&A and corporate core competitiveness

What is the corporate core competitiveness

Foster and enhance the core competitiveness of the strategic thinking

Why should we enhance the core competitiveness

Lacking of the core competitiveness

Cultivating the core competitiveness through corporate M&A

Two methods of obtaining the core competitiveness

Core competitiveness has been the sourcing power of merge activities

Analyzing the key considerations before entering into cross border M&A

Defining key factors that play a significant role in M&A flows

Managing multi-jurisdiction due diligence

Knowledge of geographic and industrial sectors have proven most attractive and the places future opportunities lie

Understanding cultural considerations in cross border deals

Decision making process of strategic M&A

Characteristics of strategic M&A

M&A decision making process

Opportunity analysis stage

Preliminary analysis stage

Detailed analysis stage

Evaluation and decision making stage

Target selecting

Understanding the differences between business valuation on local and international M&A transactions and negotiating the best deal

What are the differences of business valuation when merging or acquiring local companies and international companies?

Similar area,finance,legal,IP,HR,etc,but with different areas of concerns

Difference in accounting,legal/IP,labor issues

Key considerations in evaluating a target company

Acquirer's business strategy vs.target business

Products&marketing

Identify synergy&improvement

Management team

Middle management

Corporate Culture

Optimizing a valuation----How to reach common understanding of the business valuation and transaction price on both sides of the fence?

Communication

Cultural factors

Trust

Control misunderstanding and misleading information

Case studies-Lessons learned

Examining the synergies after strategic M&A-Case study from listed companies

Management synergy

Operating synergy

Diversification synergy

Financial and tax synergy

Intangible assets synergy

Case Study-Advancing the negotiation and closing the deal

Negotiating tactics:How to position your company from the opening offer to final agreement

Using due diligence to enhance your advantages

Understanding the strengths and the weaknesses in the other side's position

Identifying the key value drivers

Management Buyout

The development of MBO

The purpose of MBO

The financing method of MBO

The pricing strategy of MBO

Case study

想了解最新詳細課程大綱及資料,點擊網頁左側的在線咨詢圖標,與在線老師交流咨詢領取。

Accenture research shows that more than 70%business results will be influenced by outstanding finance function.Any enterprise doesn’t achieve the finance function transforming will definitely be threatened in nowadays fierce competition for lacking of decision support.As qualified finance executives,we should simplify the underlying business process,increase the time of decision-making support.Worldwide top companies have seized the opportunity to transform the finance function to achieve more effective financial work,then how about you?

This course invites Dr.Alan Parkinson,the well-known professor of University College London,to be the honorable lecturer on presenting the impacts of the changing world on finance function,and raising the response of finance function to the external influences.Alan will also guide the finance executives to utilize‘DMAIC Principle’(Define,Measure,Analyze,Improve,and Control)for optimizing company’s finance process.This course will help companies create values from customers’perspective and implement effective financial reform for enhancing competitive advantages.

?Knowing current worldwide changes and their major influence on finance function

?Understanding the finance function solutions for coping the changes and the development tendency of finance accounting

?Learning‘DMAIC Principle’for optimizing the finance process

?Strengthening data mining and acknowledgement

?Building partnership between finance and management level

?Enhancing value creation from customers’perspective

CFO

Finance Director

Chief Accountant

Finance Manager

Finance/Accounting Personnel

Day 1 |

-The implications of a changing world for the Finance function -Tasks of Accountants -Changes in The Organisational World -Manual Workers vs Knowledge Workers -The Impact on the World of Accountants Finance in the Future -The Shift in Focus within Finance -Better Performance Through Better Finance Support -Finance and IT Interfaces -Changing Information Demands Improve the Finance process:Inputs into Outputs -‘Business Partners’ -‘Lean’methodology -Undesirable effects(UDE’s) -Force field analysis Balanced scorecards -BSC KPIs -BSC Mechanisms -Practical Application -Advice For Successful Implementation -The Efficiency/Effectiveness Matrix Key performance indicators -Measuring Efficiency,Effectiveness,Economy -The 3Es&VFM -Holistic Measures -The Efficiency/Effectiveness Matrix |

Day 2 |

USING BUDGETS TO MANAGE AND PLAN:Beyond Conventional Budgeting -STRATEGIC CORPORATE PLAN -Budget Relationships(based on commercial business) -Traditional Budgeting -Playing Games with the Budget -The Hockey Stick -Influencing behaviorthrough responsibility accounting -The Utility of Budgets From‘Old’to‘New’Budgeting -Alternative Business Structures -Six Principles of Devolved Leadership -Unsuitability of Budgets -Six Adaptive Processes Thoughts about costs -Another Way of Looking at Costs -Full Costing -Contribution Costing‘Contribution Significance’in Your Area -Activity Based Costing and Illustration -Cost Pools Variances from Budgets -Making Sense of Budget Variances -Investigating Variances |

想了解詳細課程資料,點擊網頁左側的在線咨詢圖標,與在線老師交流。

What do you want to achieve or avoid?The answers to this question are objectives.How will you go about achieving your desire results?The answer to this you can call strategy.

Managing changing market conditions is never easy,but turmoil also presents unique opportunities to acquire previously unobtainable targets.However,acquirers must understand today’s credit limitations,new competition and investment legislation,increasing shareholder activism,and merger and acquisition(M&A)litigation issues.

The downturn may present many acquisition opportunities,but which fit best with your long-term business strategy?Leading strategic planners will describe how to develop an effective investment strategy,identify potential targets,and efficiently evaluate opportunities.Through this training you will explore how to identify and assess strategic targets,evaluate investment opportunities,navigate today’s deal hurdles,and successfully integrate an acquired business to deliver real results and real value.

Ensuring the realization of the M&A purpose

Deeply analysis on the hottest topics of M&A

Understanding the obstacles of Chinese corporations to do the strategic merge&acquisition

Learning the laws and regulations involving in the merge&acquisition activities

Controlling the risks when formulating a merge&acquisition strategy

Developing M&A deal negotiation skills

Gaining knowledge of target sourcing and driving success in the down market

Advancing in evaluation models and methods

Improving assessment of risk

Obtaining strategies of finance in M&A

CEO,VP,Director,GM,Head and Manager of

Strategic Planning、Finance

Corporate/Business Development

M&A/Legal

Corporate development strategy vs. M&A strategy

- Stable development strategy

- Defense strategy

- M&A categories

- Transaction valuation

- M&A Financing methods

- Case studies

Ensuring the new business conforms to company's objectives

- Differentiating Transaction Success & Deal Success

- Understanding the main factors for value creation

- Reorganizing, reconstructing and adjusting the business system

- Recommendation for PMI (Post Merger Integration) strategy

Strategic M&A and corporate core competitiveness

- What is the corporate core competitiveness

- Foster and enhance the core competitiveness of the strategic thinking

- Why should we enhance the core competitiveness

- Lacking of the core competitiveness

- Cultivating the core competitiveness through corporate M&A

- Two methods of obtaining the core competitiveness

- Core competitiveness has been the sourcing power of merge activities

Analyzing the key considerations before entering into cross border M&A

- Defining key factors that play a significant role in M&A flows

- Managing multi- jurisdiction due diligence

- Knowledge of geographic and industrial sectors have proven most attractive and the places future opportunities lie

- Understanding cultural considerations in cross border deals

Decision making process of strategic M&A

- Characteristics of strategic M&A

- M&A decision making process

- Opportunity analysis stage

- Preliminary analysis stage

- Detailed analysis stage

- Evaluation and decision making stage

- Target selecting

Understanding the differences between business valuation on local and international M&A transactions and negotiating the best deal

- What are the differences of business valuation when merging or acquiring local companies and international companies?

- Similar area, finance, legal, IP, HR, etc, but with different areas of concerns

- Difference in accounting, legal/IP, labor issues

- Key considerations in evaluating a target company

- Acquirer's business strategy vs. target business

- Products & marketing

- Identify synergy & improvement

- Management team

- Middle management

- Corporate Culture

- Optimizing a valuation----How to reach common understanding of the business valuation and transaction price on both sides of the fence?

- Communication

- Cultural factors

- Trust

- Control misunderstanding and misleading information

- Case studies-Lessons learned

Examining the synergies after strategic M&A-Case study from listed companies

- Management synergy

- Operating synergy

- Diversification synergy

- Financial and tax synergy

- Intangible assets synergy

Case Study-Advancing the negotiation and closing the deal

- Negotiating tactics: How to position your company from the opening offer to final agreement

- Using due diligence to enhance your advantages

- Understanding the strengths and the weaknesses in the other side's position

- Identifying the key value drivers

Management Buyout

- The development of MBO

- The purpose of MBO

- The financing method of MBO

- The pricing strategy of MBO

- Case study

想了解最新詳細課程大綱及資料,點擊網頁左側的在線咨詢圖標,與在線老師交流咨詢領取。

超市聯營是指超市與供應商聯合經營的項目,由供應商提供商品,由超市提供場地和收銀的,此時超市銷售商品實際上是代銷商品,相關的賬務處理怎么做?

超市聯營商品的賬務處理

1、收到商品時,會計分錄:

借:受托代銷商品

貸:受托代銷商品款

2、銷售時,會計分錄:

借:銀行存款

貸:主營業務收入

應交稅費—應交增值稅(銷項稅額)

借:主營業務成本

貸:受托代銷商品

3、收到增值稅專用發票時,會計分錄:

借:受托代銷商品款

應交稅費—應交增值稅(進項稅額)

貸:應付賬款

4、支付貨款:

借:應付賬款

貸:銀行存款

聯營企業分得的利潤的會計分錄

1、采用權益法核算的

資產負債表日,企業應按被投資單位實現的經調整的凈利潤或凈利潤計算享有的份額:

借:長期股權投資——損益調整

貸:投資收益

聯營公司宣告分配股利時,需要沖減損益調整科目:

借:應收股利

貸:長期股權投資——損益調整

正式收到時:

借:銀行存款

貸:應收股利

2、采用成本法核算的

企業應按被投資單位宣告發放的利潤或現金股利中屬于本企業的部分入賬:

借:應收股利

貸:投資收益

收到投資利潤:

借:銀行存款

貸:應收股利

受托代銷商品是什么?

受托代銷商品是指接受他方委托代其銷售的商品,受托方并沒有取得商品所有權上的主要風險和報酬,不符合資產的定義。因此,代銷商品應作為委托方而不是受托方的存貨處理,不能確認為受托方的資產。

What management and leadership skills do the most successful Senior Executives possess?What are the qualities and characteristics of the ideal finance leader?Recently,CFO Research Services,in collaboration with Tatum,surveyed 250 senior finance executives at North American companies on the non-technical business management and leadership skills that finance executives not only under pressure to manage financial compliance,processes,and controls in an environment of intense regulatory scrutiny,but also need to meet the demands of an expanded business mandate.

Indisputably,broad management training will help senior executives manage and support the business,however they also seek training on industry and competitive dynamics,business management,and the skills often labeled as‘soft skills’-collaboration,negotiation,and communication.

This training will offer practical guidance to Senior Executives on how to consolidate and promote their financial leadership by adopting the advanced leadership outcome model and the applicable financial signatures,as well as explore on how performance management and decision making are being embraced throughout companies and in diverse business categories.Through presentations from leading thought leader and cutting-edge case studies,this training will highlight the extensive reach of the achievement of enterprise’s valuation goals.

A Revolutionary new approach to Executive assessment with a full suite of evaluation instruments

Increasing the valuation of the enterprise by choosing the right alignment process to best achieve the enterprise’s valuation goals

Enabling your top executives to understand the potential of their own financial profile to improve the enterprise’profitability and valuation and align their operational mission to the enterprise valuation goals.

Understanding how to identify,select,and retain executives with a winning financial signature

Strengthening enterprise Human Resource processes by implementing the correct HR processes for achieving the targeted level of profitability

Turning analytics into action for gaining the ability to change course in volatile circumstances as well as a true competitive advantage

Taking a methodical approach to improving decision making to boost revenue,shareholder return,and return on invested capital

C-level including CEO,CFO,COO,CMO,Chief Human Resources Officer,Chief Learning Officer

Line executives and managers including Vice-Presidents,P&L managers,General Managers

Training and development executives,including leadership development managers

Human resource executives including HR heads,recruitment,succession planning executives

Chapter 1 | Chapter 2 |

-The Leadership Outcome Model -Identifying and Measuring Financial Style and Personality -The components of Financial Style and Personality -Work group 1:Buying Mission Exercise -Financial Signatures and Missions -The Nine Financial Signatures -How Financial Signature is impacted by Corporate Strategy -Work group 2:Team Financial Style Simulation -Are there Good and Bad Financial Signatures? -Financial Signature and Executive Performance -Strategy and Innovation -Operations -Sales -Quality -Customer Service -Valuation and Financial Mission -Defining the Financial Mission of an Executive -Why Financial Signature and Mission Differ -The Components of Financial Mission -Alignment of Financial Mission with Team,Business Unit and Company Financial Missions -Work group 3:Company Financial Style and Valuation Simulation | -Maximizing Your Financial Performance -Turing Analytics into Action -Four Dimensions of Decision Making and Execution -Five Step Process for improving decision effectiveness -Financial Mission and Business Strategy -Work group 4:Valuation Impact of the CEO Exercise -Macroeconomic and Microeconomic Impacts of Financial Signature -Company Evolution -Capital Intensity -Market Evolution -Competitive Dynamics -Market Capitalization and Valuation -Work group 5:Competitive Simulation -Improving Leadership Outcome -Leadership Outcome Type and Financial Mission -Financial Mission and Career Success -Financial Mission and Leadership Agility -Changing Financial Mission -Work group 6:Leadership Outcome Simulation -Case Study–Financial Mission and Outcome -Work group 7:Coaching Simulation -Conclusions in Financial Leadership |

想了解最新詳細課程大綱及資料,點擊網頁左側的在線咨詢圖標,與在線老師交流咨詢領取。

眾所周知,ACCA是一門國際類財會考試,試卷中的題目基本都是全英文的,部分國內考生有的會看不懂題目、有的會看不懂選項,對此,會計網出一道F1階段的經典例題,為大家分享當中的解題技巧。

經典例題訓練")

Question

Which one of the following statements is true?

A:Limited company status means that a company is only allowed to trade up to a predetermined turnover level in any one year.

B:For organisations that have limited company status, ownership and control are legally separate.

C:The benefit of being a sole trader is that you have no personal liability for the debts of your

business.

D:Ordinary partnerships offer the same benefits as limited companies but are usually formed by professionals such as doctors and solicitors.

(題目摘自BPP練習冊paper F1)

這道題考的是三種不同legal status的組織,分別是sole trader, partnership, limited companies,我們來逐一看下四個選項。

A選項:

有限責任公司這種法律實體意味著一個公司在任何一年僅僅被允許創造一個提前規定的營業額水平,這個說法是不對的,因為這種法律實體只是說在法律上有獨立的法人資格,并沒有規定營業額的水平。

B選項:

有限責任公司這種實體在法律上的擁有權和控制權是分離的。這個是對的,有限責任公司最大的特點就是separate legal personality from its owners(shareholders)。比如說你是某個公司的股東,當初你入股100萬,如果現在公司破產了,你只需要承擔這100萬的損失,其他的債務都不會由你來承擔。

C選項:

個體戶的優點就是你不需要為了你的公司背負個人債款,這個是不對的,因為sole trader的擁有者跟他的企業在法律上不能實現分離,因此公司的盈虧和個人的利益是捆綁在一起的,所以一旦公司破產,個人也需要承擔巨額的債務。

D選項:

普通合伙制和有限責任公司的優點一樣,但是一般是由一些專業團體組成,例如醫生和律師。這個是不對的,合伙制和有限責任公司的優點是不一樣的,普通的合伙制也不能實現法律上與擁有者的分離。在之后的F4科目里面,我們會學到其他類型的合伙制,例如Limited Liability Partnership(LLP)有限責任合伙,這種類型的合伙制就類似于有限責任公司,可以實現法律上的獨立法人資格。

所以,最后答案是:B,你答對了么?

來源:ACCA學習幫

在備考ACCA過程中,考生除了理解好教材上每一個考點外,通過做題練習來進行鞏固也是必不可少的重要環節,今天,會計網針對F1階段為大家帶來一道經典例題,同時講解考題當中的重難點內容。

Question:

Which one of the following statements is true?

A Limited company status means that a company is only allowed to trade up to a predetermined turnover level in any one year.

B For organisations that have limited company status, ownership and control are legally separate.

C The benefit of being a sole trader is that you have no personal liability for the debts of your

business.

D Ordinary partnerships offer the same benefits as limited companies but are usually formed by professionals such as doctors and solicitors.

(題目摘自BPP練習冊paper F1)

Answer:

正確答案:B

這道題考的是三種不同legal status的組織,分別是sole trader, partnership, limited companies,我們來逐一看下四個選項。

A選項,有限責任公司這種法律實體意味著一個公司在任何一年僅僅被允許創造一個提前規定的營業額水平,這個說法是不對的,因為這種法律實體只是說在法律上有獨立的法人資格,并沒有規定營業額的水平。

B選項,有限責任公司這種實體在法律上的擁有權和控制權是分離的。這個是對的,有限責任公司最大的特點就是separate legal personality from its owners(shareholders)。比如說你是某個公司的股東,當初你入股100萬,如果現在公司破產了,你只需要承擔這100萬的損失,其他的債務都不會由你來承擔。

C選項,個體戶的優點就是你不需要為了你的公司背負個人債款,這個是不對的,因為sole trader的擁有者跟他的企業在法律上不能實現分離,因此公司的盈虧和個人的利益是捆綁在一起的,所以一旦公司破產,個人也需要承擔巨額的債務。

D選項,普通合伙制和有限責任公司的優點一樣,但是一般是由一些專業團體組成,例如醫生和律師。這個是不對的,合伙制和有限責任公司的優點是不一樣的,普通的合伙制也不能實現法律上與擁有者的分離。在之后的F4科目里面,我們會學到其他類型的合伙制,例如Limited Liability Partnership(LLP)有限責任合伙,這種類型的合伙制就類似于有限責任公司,可以實現法律上的獨立法人資格。

來源:ACCA學習幫

ACCA考試的知識體系范圍非常廣泛,幾乎涵蓋了整個財會領域,考生在學習過程中將所學知識點遺忘也是在所難免的事情。下面會計網針對F6階段整理了大家容易忘記的知識點,我們來看看吧。

易忘知識點匯總")

IHT

1. IHT的AE不要忘記它!而且可能會有去年帶過來的哦!

2. 生前轉讓的生前稅計算,抵減nil band 的是:轉讓當日前7年的CLT的GCT金額!

3. 生前轉讓的死亡稅計算,抵減nil band 的是:轉讓當日前7年的CLT 和要交死亡稅的PET,都是GCT金額!可能有tapper relief,CLT,計算死亡稅的時候還要減掉交過的生前稅。

4. 死亡遺產的遺產稅計算,抵減nil band 的是:去世當日前7年的CLT和PET ,都是GCT金額!

5. GCT = 轉讓金額 – 可以用的抵減(AE等)+ 贈予方交的生前稅

6. 轉讓nil band,使用方去世當年的nil band * 配偶去世時未使用完的比例

7. 去世的時候residence nil band 只要沒有用,都可以轉移給配偶。

VAT

1. 未來測試是看未來30天的收入,一定要有合理的理由預測才可以,歷史測試看的是過去12個月!注意未來測試注冊生效日是測試日哦!

2. 壞賬到期之后六個月計提input 調整回來。注意VAT相關題目,一定要看,數字是含稅的還是不含稅!

3. 第一次晚交只產生觀察期,在觀察期當中晚交,延長觀察期并可能要交罰款。

個人稅收征管 (17/18)

1. 交Return的時間

紙質:稅務局通知日+3個月 和 2018.10.31 二者取晚

電子:稅務局通知日+3個月 和 2019.1.31 二者取晚

2. Return交晚的罰款

≦ 3 months ?100

3-6 months ?100 + ?10 per day (for a maximum of 90 days)

6-12 months ?100+?10*90+ 5% of tax due (最后一項 最少?300)

3. Return 修改

Taxpayer: 2020.1.31之前可以修改

HMRC : 真正上交日 + 9 months

4. Return 錯誤罰款

少算的稅款乘下表中的比例

易忘知識點匯總")

5. 繳稅款

POA : 2018.1.31,2018.7.31

基于16/17 的tax 及class4 計算,少于1000不用交

BP:2019.1.31

6. 稅款交晚

POA 交晚只有罰息

BP交晚 有罰息和罰款

7. 記錄保持

有TI 或者PBI的納稅人: 所有記錄保持到2024.1.31

其他納稅人:2020.1.31

未保持罰款最多?3,000

8. Compliance check

Return按時交:

真正上交日 + 12 months

Return晚交:

真正上交日之后的Quarter day + 12 months

(31 January, 30 April, 31 July and 31 October)

企業稅收征管 (17/18)

1. 交Return 的時間

稅務局通知日+3個月 和 POA會計期間截止之后的一年 二者取晚

2. Return交晚的罰款

易忘知識點匯總")

3. Return 修改

Company amend: 應該上交日 + 12 months

HMRC amend: 真正上交日 + 9 months

4. Return 錯誤罰款 同個稅

5. 繳稅款

小公司:AP + 9 months +1 day

大公司:注意判定條件,分期付款交稅

AP 開始后的7th month 14th, 10th month 14th, 13th month 14th ,16th month 14th

Each instalment = 3 *CT/m

6. 稅款交晚 只有罰息

7. 保持記錄

以下三個時間取晚:

- AP結束后六個月

- compliance check 做完

- 通知要做compliance check的日期但是該compliance check最終沒有做

未保持罰款最多?3,000

8. Compliance check

Return按時交:

Group companies: 應該上交日 + 12 months

Other companies: 真正上交日 + 12 months

Return晚交:

真正上交日之后的Quarter day + 12 months

(31 January, 30 April, 31 July and 31 October)

來源:ACCA學習幫

2023年CFA學生獎學金申請時間為:2022年9月1日08:00—2023年7月31日23:59,CFA獎學金還有勵志獎學金、女性獎學金、教授獎學金、監管機構獎學金以及媒體獎學金。其中媒體獎學金已經不再接受新的申請者。

1、Access Scholarship(勵志獎學金)

適用人群:對于無法負擔報名費用的考生,且申請人必須要滿足CFA課程的入學要求;

獎勵金額:免注冊費,考試費減免至250美元

2、Women’s Scholarship(女性獎學金)

適用人群:對于有興趣獲得CFA章程,但是沒有資格獲得其他獎學金的女性;

獎勵金額:免注冊費,考試費減免至350美元

3、Student Scholarship(學生獎學金)

適用人群:適用于目前就讀于附屬大學(affiliated university)的學生;

獎勵金額:免注冊費,考試費減免至350美元

4、Professor Scholarship(教授獎學金)

適用人群:適用于在合格機構教授,且符合最低學分要求的全日制學院/大學的教授/行政人員/部門負責人。

獎勵金額:免注冊費,考試費減免至350美元

5、Regulator Scholarship(監管獎學金)

適用人群:適用于金融監管機構、證券委員會、合格證券交易所、中央銀行、安全組織或政府實體的員工。具體來說,是那些監督或規范投資管理行業的運營、實踐標準或商業行為并與CFA協會簽訂計劃協議的實體。

獎勵金額:免注冊費,考試費減免至350美元

6、Media Scholarship(媒體獎學金)

媒體獎學金暫時不再接受新的申請者

1、進入到CFA協會官網的獎學金申請界面,申請人可點擊對應的獎學金項目;

2、完成賬號登錄之后,點擊View programs,之后在對應的獎學金下方點擊MORE;

3、點擊APPLY,開始進行獎學金申請;

4、點擊獎學金申請列表,之后進入到具體的申請界面;

5、閱讀申請政策,接受并點擊NEXT;

6、根據要求填寫信息;

7、檢查填寫的全部信息,確認無誤之后,即可點擊SUBMIT提交申請。

1、無論考生申請何種獎學金,都要求未進行考試報名的任何操作;

2、獎學金申請成功后減免的報名金額不包括考生居住地適用的增值稅(VAT)、商品和服務稅(GST)或其他銷售稅(sales tax);

3、申請者可以選擇適合個人情況的獎學金去申請,如果同時申請多個獎學金,每次考試僅能獲得一次獎學金發放,適用的減免金額將以最新發布的獎學金信息為準。

在ACCA考試中,AC科目的客觀題選項經常會出現比較多陷阱來迷惑大家,而解答客觀題最常見的技巧就是使用排除法。對此,會計網今天帶來AB科目兩道經典例題,教大家如何使用排除法進行解答。

Question 1:Which one of the following statements is true?

A Limited company status means that a company is only allowed to trade up to a predetermined turnover level in any one year.

B For organisations that have limited company status, ownership and control are legally separate.

C The benefit of being a sole trader is that you have no personal liability for the debts of your business.

D Ordinary partnerships offer the same benefits as limited companies but are usually formed by professionals such as doctors and solicitors.

正確答案:B

被題目嚇到?不存在的。這道題考的是三種不同legal status的組織,分別是sole trader, partnership, limited companies,我們來逐一看下四個選項。

A選項,有限責任公司這種法律實體意味著一個公司在任何一年僅僅被允許創造一個提前規定的營業額水平,這個說法是不對的,因為這種法律實體只是說在法律上有獨立的法人資格,并沒有規定營業額的水平。

B選項,有限責任公司這種實體在法律上的擁有權和控制權是分離的。這個是對的,有限責任公司最大的特點就是separate legal personality from its owners(shareholders)。比如說你是某個公司的股東,當初你入股100萬,如果現在公司破產了,你只需要承擔這100萬的損失,其他的債務都不會由你來承擔。

C選項,個體戶的優點就是你不需要為了你的公司背負個人債款,這個是不對的,因為sole trader的擁有者跟他的企業在法律上不能實現分離,因此公司的盈虧和個人的利益是捆綁在一起的,所以一旦公司破產,個人也需要承擔巨額的債務。

D選項,普通合伙制和有限責任公司的優點一樣,但是一般是由一些專業團體組成,例如醫生和律師。這個是不對的,合伙制和有限責任公司的優點是不一樣的,普通的合伙制也不能實現法律上與擁有者的分離。在之后的F4科目里面,我們會學到其他類型的合伙制,例如Limited Liability Partnership(LLP)有限責任合伙,這種類型的合伙制就類似于有限責任公司,可以實現法律上的獨立法人資格。

Question 2:Calum , Heidi and Jonas are managers for Zip Co. They have been told that their salary will be based on company performance and that a bonus scheme will also be introduced. The bonus will also be related to company performance. Which of the following best describes the approach to governance that Zip Co is using?

A Stewardship theory B Agency theory C Stakeholder theory

正確答案:B

這道題題干很長,保持耐心跟著Vicky一起讀題,C,H,J都是Z公司的經理,他們的工資都是基于公司的業績以及引入了一個獎金機制,獎金也是跟公司的業績相關的。然后問下列哪個是Z公司正在用的理論?我們來逐一看下三個選項。

A選項, Stewardship theory,管家理論----公司的管理層被視為公司的管家,管家總是一心為東家著想的角色,因此管家跟公司的整體戰略方向一致,所以不存在管理層和股東之間利益的矛盾沖突。所以也不需要題目中的獎勵機制來促進兩者的目標一致。因此A不對。

B選項, Agency theory,代理理論---公司的擁有者(股東)被視為當事人,公司的管理者被視為代理人,管理層被股東任命去代理公司的管理事項,那么管理層自然想要為自己的利益著想,而管理層的利益一般都是短期的,而股東想要追求的是公司長期的利益,想要讓公司長期發展下去,這個時候就會產生矛盾沖突。然后題目中的獎勵機制可以幫助兩者目標一致,因此B選項是最合適的。

C選項, Stakeholder theory,利益相關者理論---管理層對利益相關者有duty of care,意思是管理層有責任關心所有利益相關者的利益,而不僅僅是股東的利益,所以跟題目也不匹配。

來源:ACCA學習幫

CFA獎學金類型及獎勵金額說明如下:

1、Access Scholarship(勵志獎學金)

適用人群:針對交不起報名費的考生,且申請人必須符合CFA課程的入學要求;

獎勵金額:免注冊費,考試費減免至250美元

2、Women’s Scholarship(女性獎學金)

適用人群:對于有興趣獲得CFA證書,但不具備其他獎學金資格的女性;

獎勵金額:免注冊費,考試費減免至350美元

3、Student Scholarship(學生獎學金)

適用人群:適用于目前就讀于附屬大學(affiliated university)的學生;

獎勵金額:免注冊費,考試費減免至350美元

4、Professor Scholarship(教授獎學金)

適用人群:適用于在合格機構教授,且符合最低學分要求的全日制學院/大學的教授/行政人員/部門負責人。

獎勵金額:免注冊費,考試費減免至350美元

5、Regulator Scholarship(監管獎學金)

適用人群:適用于金融監管機構、證券委員會、合格證券交易所、中央銀行、安全組織或政府實體的員工。具體來說,是那些監督或規范投資管理行業的運營、實踐標準或商業行為并與CFA協會簽訂計劃協議的實體。

獎勵金額:免注冊費,考試費減免至350美元

6、Media Scholarship(媒體獎學金)

媒體獎學金暫時不再接受新的申請者。

申請步驟一步:進入官網,進入CFA項目獎學金項目

步驟二:點擊進入申請頁面

步驟三:選擇獎學金申請

步驟四:選擇申請的獎學金

步驟五:填寫個人基本信息,*部分為必填信息(填寫各種個人信息:郵箱、地址、電話聯系信息)。

步驟六:填寫您的聯系信息

第七步:填寫支持和了解您情況的兩個聯系人的信息,不包括CFA協會工作人員和CFA協會會員。

協會要求您提供兩個證人的基本信息,協會將在需要時聯系他們,核實您提供的信息的真實情況。

步驟八:填寫對你有經濟依賴的家庭成員的信息

步驟九:填寫個人和家庭收入

列出基本信息,包括你的父母、配偶、兄弟姐妹和孩子等,依靠你的收入生活。

簡而言之,講一個關于你和CFA的故事。這里特別強調,一個真實而生動的自我陳述是成功申請的法寶。

步驟十:家庭資產和投資

按年計算,系統會自動總結工資收入、配偶工資、其他業務收入、出租屋收入、養老金收入、投資債券和股票收入。

以下是CFA協會規定的利益沖突或關聯關系,所有有下列情況的申請人都需要在申請中充分披露。

(1)助學金申請人有親屬在CFA協會工作或CFA會員;

申請人聘請CFA協會工作人員為個人提供咨詢服務;

(3)目前或過去,申請人是CFA協會的工作人員或CFA協會的成員;

(4)申請人受到CFA協會的處罰;

當前申請人所從事的活動將對CFA協會產生負面影響。

CFA考生復習一級考試《職業倫理道德》科目時,應對具體知識點做到全面把握,才能穩穩拿下高分。下面會計網為大家整理了該科目的“獨立客觀性”的知識要點,趕快來看!

7種關系:

1.Buy-sideclients:基金經理等會對sell-sideanalyst威逼利誘;

2.Investment Banking Relationships:研究部要拒絕投行部等其他部門的威逼利誘(Firewall;Restricted list);

3.Public Companies:上市公司會對分析師威逼利誘,分析師要堅持自己對上市公司的看法;

4.Issuer-PaidResearch:付費報告,公司付費請分析師寫公司的研報,報告需要披露雙方的關系同時分析師只能收固定費用,任何與研究相關的bonus都不能收;

5.Selection of Fund manager and Custodian:在選擇基金經理和托管人時,不能受賄也不能行賄;

6.Performance Measurement and Attribution:負責業績歸因和核算的人要堅持自己的分析結果,不能屈服于威逼利誘;

7.Credit Rating Agency Opinions:債券評級機構對債券的評級結果不能受到發債公司的影響;

Travel Funding:

Best practice:自己付錢;例外:當所去的地方是偏遠(remote)時,可以接受對方安排;

Gift:

第三方(調研對象等):只能收modest gifts,注意disclose;

Exception:客戶的禮物(視為額外報酬,提供了服務的獎勵),都可以接受,disclose。

1.7種關系,要求能夠從給出的題干中判斷出來,并選出正確的做法。

2.差旅費的要求,禮物是否能分清不同情況的不同要求。

為增加大家的備考信心,會計網還為大家準備了一份CFA備考大禮包,想要學習更多有關CFA考試的知識,請點擊下方圖片↓,即可免費領取電子版的CFA學習資料!無論你是上班族還是全職考生,領取資料后,都可實現線上查看具體考點哦~還能有效提高分數,趕快動動手指點擊領取↓,盡情學習吧~

從2024年起,CFA ESG課程大綱的版本不再沿用之前的v1、v2版本叫法,比如2023年CFA ESG是v4版。取而代之的是全面按照年份來區分。2024年新的課程大綱即為CFA ESG v2024。

一、整體變動

2024版內容相比2023版整體縮減10%,這對于考生來講是個好消息。

整體結構保持不變,依然是9大章節。

二、章節變動

Chapter 2

第二章去掉了“ESG投資歷史”部分,這表明協會致力于關注當下最新內容。(見下圖)

Chapter 3

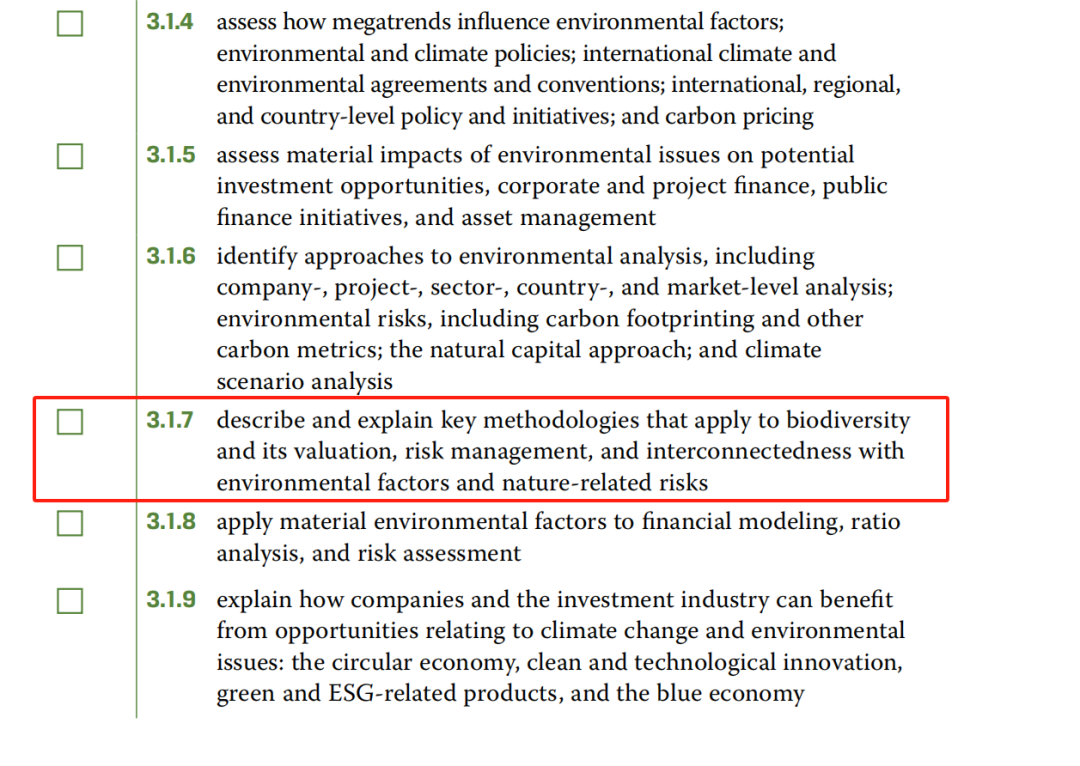

在第三章“環境因素”中,2024年大綱增加了有關生物多樣性的內容,包括其評估、風險管理以及與環境因素和自然相關風險的相互關聯性。(3.1.7)(見下圖)

Chapter 6

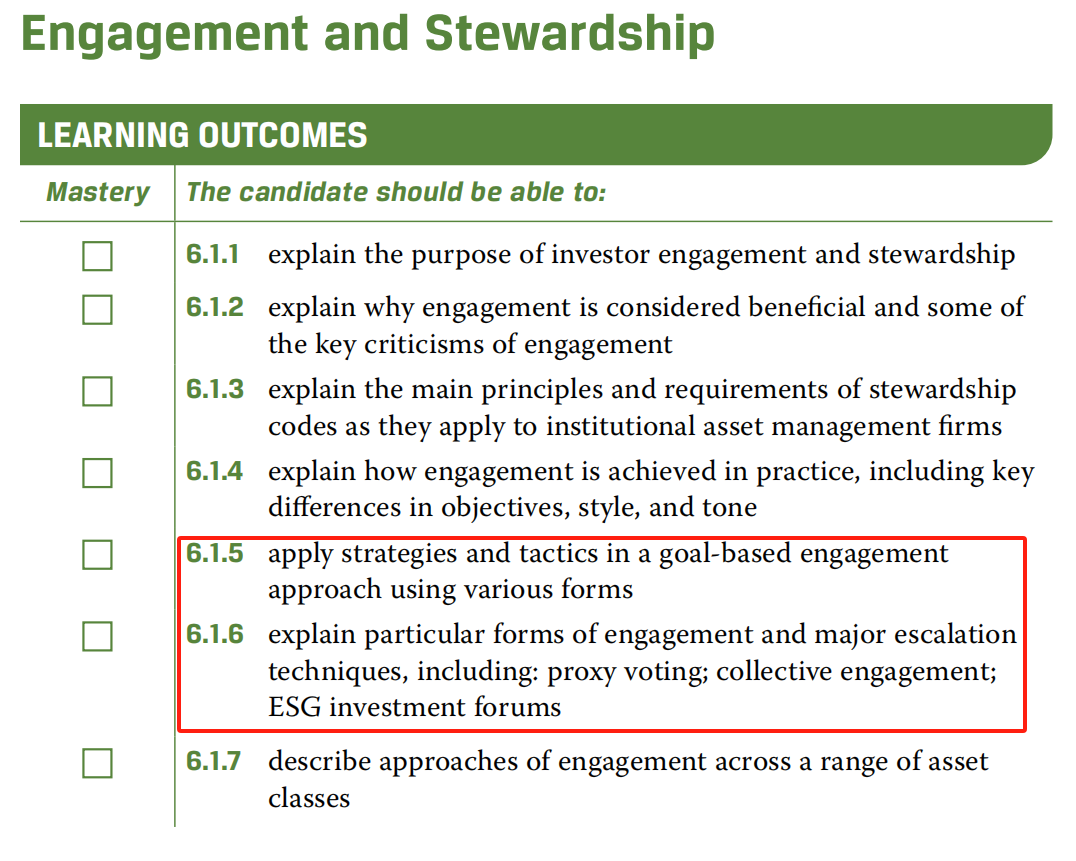

在第六章“參與和管理”中,2024年大綱細化了參與策略和戰術的應用,并說明了特定參與形式和主要升級技術,包括代理投票、集體參與和ESG投資論壇。(6.1.5和6.1.6)(見下圖)

Chapter 7

第七章是此次大綱修訂變化最大的部分。整章內容進行了重組,2023版本的21個小節內容大幅縮減為2024版的14個小節,可以理解為縮減了幾乎三分之一的內容。

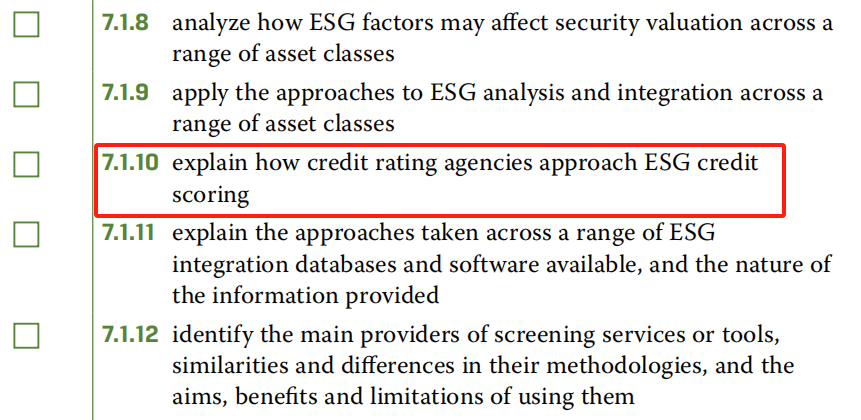

在第七章“ESG分析、估值與整合”中,2024年大綱對整合ESG分析到投資過程的描述進行了簡化,并且增加了對信用評級機構處理ESG信用評分的解釋。(7.1.10)(見下圖)

Chapter 8

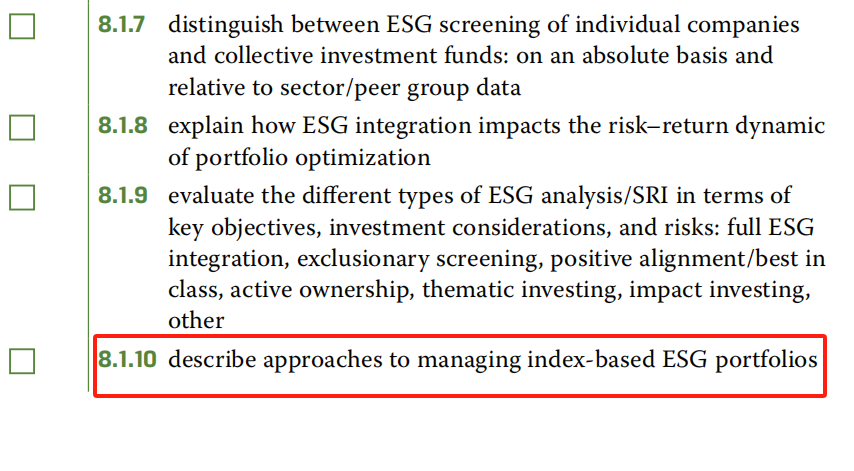

在第八章“綜合投資組合構建與管理”中,2024年大綱對管理基于指數的ESG投資組合的描述做了細微調整。(8.1.10)(見下圖)

Chapter 9

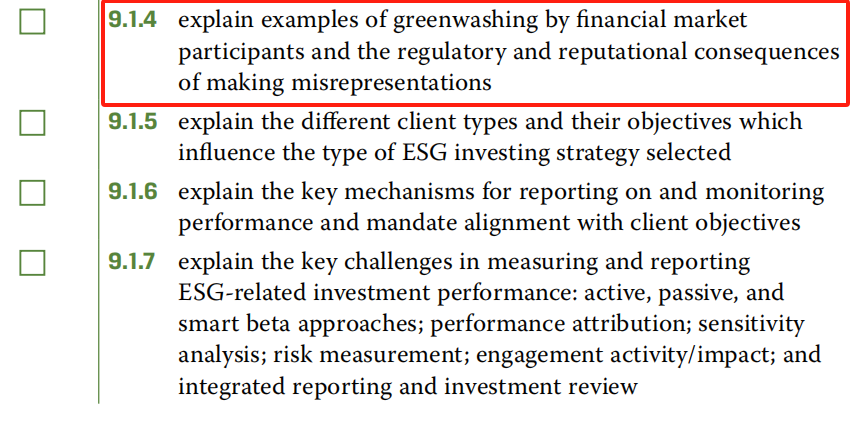

在第九章“投資任務、投資組合分析與客戶報告”中,2024年大綱新增了對金融市場參與者“漂綠”行為及監管和后果的內容,反映出業界對于ESG聲明真實性的嚴格審查,以及解決ESG行業內漂綠行為的日益重要性,幫助考生在日后的工作中應對此種復雜問題的準備(9.1.4)(見下圖)

三、2024考試大綱權重變化

Topic | 2024 Topic Weight | 2023 Topic Weight |

Introduction to ESG Investing | 7% | 8-15% |

The ESG Market | 6% | |

Environmental Factors | 12% | 8–15% |

Social Factors | 12% | 8–15% |

Governance Factors | 11% | 8–15% |

Engagement and Stewardship | 9% | 5–10% |

ESG Analysis, Valuation and Integration | 21% | 20–30% |

Integrated Portfolio Construction and Management | 13% | 10–20% |

Investment Mandates, Portfolio Analytics, and Client Reporting | 9% | 5–10% |

從考綱權重對比情況來看(見上圖),協會對于ESG知識點考察更加精細,可以直接精確到題目的數量。

目前來看,第7章和第8章以及ESG三要素的考點占據多數。考生們對于這幾個章節的復習也應該投入更多時間和精力。

四、2024 Curriculum更新

CFA協會剛剛正式發布了2024版curriculum的更新內容,9個章節均有調整。主要增加了新的案例分析、新的數據圖表和更多的練習題。

如第一章 更新內容:

Key Enhancements

·ESG 2024(v5)Chapter 1 includes 33 total practice questions,featuring 8 additional Practice questions vs.2023(v4).

New Content

·Update on Blackrock’s implementation of 2020 ESG commitments

·34%of world’s largest companies committed to Paris Agreement

·Added Brazilian example to water depletion case study

·Noted costs for corporate issuers and institutional investors for climate-related disclosures and reporting

·Updated growth of new PRI signatories

·Recognized launch of ISSB reporting standards for 2024

Removed Content

·Exhibit 3–Guide to ESG reporting that was simplistic and duplicitous

·Exhibit 5 illustrative/hypothetical example of benchmarking that was poorly constructed by MSCI

·Coca-Cola water depletion case study example from 2004

·2014 study analyzing data from the global climate database provided by CDP

·“estimated that companies experience an average internal rate of return of 27%–80%on their low-carbon investments”

·2014 reference to Walmart increasing their fleet efficiency by 87%

·Reduced greenwashing references as there is new content in other chapters

·Explanation of what a meta-analysis is

LOS related

·No changes

完整版esg大綱查看:2024年CFA-ESG考試大綱

ESG考試常見問題答疑

一、官網注冊并繳費

2024年考試費為865美金,重考費690美金

考生可另外支付135美元與運費來獲得紙質版的教材。

中國內地暫無線下考試考點,但可選擇線上考試。

報名時需要選擇CFA Hongkong協會進行掛靠。

ESG退費政策:

可在付款后14天內(至東部時間第14天晚上11:59)全額退還注冊費。初始注冊不包括為重新安排由考生推遲或由CFA協會推遲的考試而進行的注冊。由于匯率波動,CFA協會不能保證支付給CFA協會的確切金額將以美元以外的貨幣退還。

二、報名時間

ESG投資證書考試無固定考季,支持線上考試,隨時報名,隨時約考,即時出成績。

題目:CFA協會ESG投資證書考試包括100道選擇題(英文)。

時長:2小時20分鐘內完成

溫馨提示:注冊后,有長達6個月的時間來安排和參加Prometric考試。

報名入口:CFA協會官網(網址:https://www.cfainstitute.org/)

三、預約考試

完成注冊后,考生最多能有6個月的時間預約考試。

四、考試形式

100道單項選擇題(3個選項),時長2小時20分鐘。考試結束后可立即得到結果:通過/未通過,稍后在CFA賬戶中也會提供(考試不允許使用計算器)。

以上就是全部內容,想要了解更多關于CFA ESG相關政策,請訪問【報考指南】欄目!一鍵輕松GET CFA ESG報名、考試費用、考試動態、證書等全面信息!

在一般情況下,acca考試的f3科目建議備考時間為2-3個月。學習本課程需要掌握財務報告的背景及目的;復式記賬法和會計系統的使用;記錄各項交易和事件;編制試算平衡表;編制基本財務報表;編制簡單的合并財務報表。學習時要對會計原理的掌握達到較為深刻的理解,要回歸考點,同時注意對題目的練習。

acca f3科目備考經驗:

1.基本的和常用的公式要記牢,比如capital、NCA等等

2.大題要仔細看清楚題目,尤其是計算題不要忘記條件如NCI、retain earning、profit

3.講義上的知識點要認真看仔細,不要忽略任何細節

4.多練題,尤其是自己不熟悉的題型

5.考試過程中不要糾結一道不會的題目浪費時間

6.講義和BPP上的習題要做,尤其是老師挑出來的題目

7.合并報表的題大家可以看看老師給的資料,上面的知識點特別詳細

8.認真對待每一次測驗,錯題要及時解決,補充知識點

9.文字題有的可以通過排除法選答案,比較靈活,要理解透徹

10.Cash book和bank balance要看好是在Dr方還是在Cr方的余額

acca f3科目的考試全部都是機考(線上),答題時間為兩個小時,均為客觀題回答。

考試試卷分為兩個部分:

Section A(共70分。35道題,每道題2分)

Section B(共30分。2道題,每題15分)

acca f3科目重點知識梳理如下:

1.合并報表的計算NCA、inventory、goodwill、retain earning、NCI

2.累計折舊的計算公式和NCA的計算公式

3.講義7-9頁的定義和公式

4.The regulatory framework各機構的職能

5.Financial information的特點

6.Source documents的內容,尤其是debit note和credit note

7.7個日記賬

8.折扣出現,買賣雙方的如何記賬

9.銷售稅要看好是否為增值稅的納稅人

10.銷售稅的計算(含稅、不含稅、折舊)

11.期末存貨的計算方法,看好題目要求

12.第八章資本化費用的內容有哪些

13.NCA折舊的計算常考,看清題目要求的折舊方法

14.NCA的處置和重估可能會結合考,大家可以做做相關習題

15.什么樣的可以成為無形資產

16.第十章的四個計算公式和影響

17.壞賬和壞賬準備對TR的影響及壞賬轉回

18.第12章83頁的表格,對資產和負債的確認

19.Right issue和bonus issue對share capital和share premium的變化

20.可贖回優先股和不可贖回優先股的區別

21.第14章會計記錄的錯誤類型、是否影響TB

22.Cash book和bank balance要看好是在Dr方還是在Cr方的余額

23.Cash book和bank balance的調節內容

24.TR、TP的T字帳dr、cr方內容

25.Gross profit margin和mark up的計算公式

26.現金流量表的計算和歌內容的歸屬

27.期后事項的調整和非調整,bankrupt、fire

28.子公司和聯營公司的確認

29.第22章合并報表重點goodwill、URP、RE等計算

30.合并報表可以多做習題

31.最后報表分析的計算公式

會計網所有內容信息未經授權禁止轉載、摘編、復制及建立鏡像,違者將依法追究法律責任。

滬公網安備 31010902002985號,滬ICP備19018407號-2, CopyRight © 1996-2025 kuaiji.com 會計網, All Rights Reserved.

滬公網安備 31010902002985號,滬ICP備19018407號-2, CopyRight © 1996-2025 kuaiji.com 會計網, All Rights Reserved.